ESOP – Achieving BEE Ownership Through Employee Share Ownership Plans

Summary: ESOPs in South Africa: Achieving B-BBEE Ownership Through Employee Ownership (TL;DR)

- Employee ownership provides an attractive option to address B-BBEE ownership in a way that can align interests and boost employee engagement and retention at the same time.

- ESOPs typically involve shareholding by a trust, through which eligible employees indirectly benefit, with scheme rules that set out the benefit and governance structure.

- If you are considering an ESOP for your business, analysing the structural options and related implications is crucial, in order to identify what makes most sense for your business and for who the targeted participants will be.

- Consideration must be given to financial outcomes (tax, accounting, company cost, employee benefit), legal implications, risks and mitigation, as well as sustainable B-BBEE compliance.

- To best managing employee expectations, simple and effective ESOP communications are important, together with trustee training.

- With over 15 years of experience in ESOP design, execution, communication and trustee training, Transcend Capital can successfully support you in identifying and implementing an optimal and sustainable ESOP solution.

ESOPs in South Africa: Achieving B-BBEE Ownership Through Employee Ownership

Employee Share Ownership Plans (ESOPs) can deliver B‑BBEE ownership recognition while aligning employee and shareholder interests and driving value creation.

This guide explores the benefits of employee ownership and explains ESOP structures in South Africa, related B-BBEE Ownership recognition requirements, accounting and tax touchpoints, the importance of strong communication, training, administration and governance, as well the Competition Commission requirements for ESOPs.

Research has identified numerous benefits of employee ownership, both for the implementing company and employees. An ESOP aligns the interests of employees and shareholders towards profitability and value creation, increases engagement, and creates a sense of ownership in the business by employees.

In South Africa, ESOPs also provide an opportunity for businesses to improve their Broad-based Black Economic Empowerment (“B-BBEE”) status through being able to recognise black ownership in the business through the ESOP. In the context of high economic inequality, employee ownership promotes economic transformation and broader participation in the economy.

In a 2021 practice note, the Department of Trade Industry and Competition (“DTIC”) confirmed the feasibility of ESOPs as an approach to address BEE ownership, which echoes previous sentiment from the DTIC as well as statements by the governing party about worker ownership.

If you are considering implementing an ESOP, it is crucial that you are clear on your objectives, understand what the available options are, and identify the optimal ESOP structure that makes the most sense for your business. One size does not fit all.

As a specialist ESOP and BEE transaction advisor to multinationals and South African corporates, Transcend Capital has advised on over 200 transactions since 2005, including various ESOPs at unlisted and listed level. Our in-depth understanding of employee ownership complexities, together with our proven corporate finance expertise and understanding of the regulatory environment means we can combine best practice with innovative thinking in finding sustainable and B-BBEE compliant ESOP solutions.

We are unique among services providers in that we provide full turnkey ESOP solutions. We have an in-depth understanding of the employee ownership process from the perspective of the scheme founder and the employee beneficiaries, allowing us to design workable ESOP structures, and create optimal communication programmes that manage employee expectations.

Benefits of an ESOP

The key drivers of ESOP implementation in South Africa has been the ability to achieve positive B-BBEE ownership outcomes in a way that provides related economic benefit ‘closer to home’ – benefitting the employees that supported business success. In terms of B-BBEE points scoring, there are certain points that are available only to broad-based ownership vehicles like an ESOP, or to limited “designated Black groups”.

A well-structured ESOP provides an opportunity to better align the interests of employees and shareholders by rewarding both groups of stakeholders for improving business performance and increasing the value of the business. Research on employee ownership has shown that there is most often higher employee engagement in an ESOPs context.

Employee ownership can also improve employee relations, as well as improve employee attraction and retention, with a related positive impact on business performance. With the skills shortage in South Africa, the ability to attract talent, reduce employee turnover as well as retain star performers is very valuable.

Successful ESOPs provide meaningful financial benefits to participating employees. Beyond increased personal wealth, from a socio-economic perspective, this increased wealth across a broad base stimulates economic activity and growth, which is ultimately good for South Africa as a whole.

How are ESOPs structured?

In South Africa, ESOPs typically hold a minority investment in companies – usually between a 5% and 25% shareholding. The size of ESOP investment will however be tailored for targeted outcomes and may be smaller or larger.

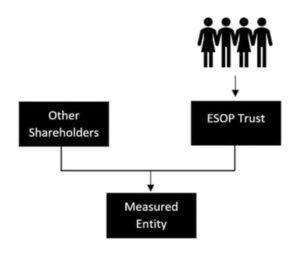

While an ESOP may well involve actual share ownership by employees, most often eligible employees participate indirectly as beneficiaries of a trust, or through an alternate intermediary vehicle.

ESOPs can be structured in many different ways and can range from being structurally simple to complex. Some schemes focus on dividend participation, some have fixed terms of life, and some are structured to be evergreen. Some “ESOPs” do not involve shareholding but involve options or phantom share schemes. While these may achieve similar goals, B-BBEE recognition outcomes may be limited.

It is important to be clear on your objectives, to consider what the available options are and what makes most sense for your business given your specific circumstances and needs.

It is also important to ensure that the chosen structure, while legally compliant, is not aggressive and does not result in risk of fronting, which is a criminal offense and carries serious implications for the company and management.

The table below sets out common structural features for ESOP:

| Legal structure |

Trust holding shares in employing company/group.

|

| Fiduciaries |

Trustees, which include founder/employer representation and employee representation.

|

| Participants |

Eligible employees, with eligibility rules being tailored by the founder to suit the desired scheme outcomes.

ESOPs can be tailored for targeted segments of the workforce eg. senior management; or all employees up to management level.

|

| ESOP term |

Either fixed-term or evergreen with termination at option of founder.

|

| Funding |

Typically, interest-bearing vendor funding from the founder, often at a discount to fair value. Funding is secured by ESOP shareholding, with some dividends being applied to loan repayment. Notional vendor funding structures are fairly common.

|

| Manner of benefit |

Manner of benefit is determined by chosen ESOP structure, taking targeted employee participants into account.

Typically employees either benefit through dividend participation or in the gain in net asset value of ESOP transactions over a defined vesting period.

Employees most often do not own shares, but rather benefit as unit-holding beneficiaries of trust.

|

| Termination of employment |

‘Good leaver’ vs ‘bad leaver’ rules, with good leavers being entitled to unvested value linked to their participation and bad leavers forfeiting value.

|

B-BBEE ownership recognition via ESOPs

Employee ownership is specifically recognised in the B-BBEE Codes of Good Practice as one of the vehicles to address BEE ownership, with bonus points being available if a qualifying ESOP is implemented.

The African National Congress has repeatedly expressed the need to broaden ownership of the economy, with extending worker ownership across the economy being a focus.

The DTIC has similarly affirmed the importance of ESOPs. A Practice Note issued by the DTIC in 2021 re-iterated that ESOPs support broad-based transformation, and can be used to achieve B-BBEE ownership recognition. In 2024 the DTIC organised the inaugral Worker Share Ownership Conference, at which President Cyril Ramaphosa welcomed the progress made with expanding worker share ownership programmes and emphasized their role in strengthening transformation of the economy and achieving the vision of the South African Constitution.

The B-BBEE Commission, tasked with over-seeing and promoting adherence with the B-BBEE Act, has previously raised some concerns regarding broad-based ownership schemes in general, but specifically had some concerns regarding ESOPs. These primarily appeared to be regarding the ability to have an evergreen (non-terminating) ESOP as well as the role of fiduciaries (eg. trustees) versus participants in decision-making. The above-mentioned Practice Note addressed these issues, and confirmed that evergreen ESOPs are acceptable, and that fiduciaries most often make decisions on behalf of the beneficiaries that they are acting in the interest of.

In order for B-BBEE ownership to be recognised via an ESOP, various requirements have to be met. The table below sets these out:

| Aspect | Requirement |

| Fiduciaries (eg. trustees for a trust) |

Employee participants must appoint at least 50% of the trustees.

|

| Beneficiaries |

The scheme constitution (eg. trust deed) must define the employee participants and their proportion of claim to receive distributions.

Fiduciaries must have no discretion in the determination of the definition of participants or of the proportion of claims to receive distributions.

|

| Operation and governance |

In order to achieve maximum points on the ownership scorecard, a track record of operating as an ESOP is required, or in the absence of such record then demonstrable evidence of full operational capacity to operate as an ESOP.

|

| Provision of information to, and engagement with participants |

The fiduciaries must present the financial reports of the ESOP at a scheme annual general meeting.

Participants must be able to participate in managing the scheme at a level similar to the management role of shareholders in a company. The scheme constitution must be available, on request, to any employee participant in an official language with which that person is familiar.

|

| On termination |

All accumulated economic interest is payable to the participants at the earlier of the date or event specified in the deed or on termination or winding up of the ESOP.

|

A critical component of B-BBEE Ownership outcomes is Net Value. It is important to structure the ESOP to not only address Net Value needs upfront, but also to address the evolving Net Value needs and targets over time.

ESOP taxation

While the government has expressed support for ESOPs, this is yet to meaningfully carry through in the tax treatment of ESOPs.

For companies implementing traditional ESOPs, there are limited opportunities for tax deductibility. With many ESOPs being vendor financed, the chosen ESOP funding structure may result in tax liabilities for the employer. It is important to be clear on the tax treatment of a proposed ESOP structure, as it can be complex and there may be opportunities to achieve similar outcomes in a more tax advantageous manner.

From the employee participant perspective, tax treatment is dependent on the scheme structure. ESOP participation may be viewed as holding restricted equity instruments, with ESOP pay-outs then being treated as taxable income in the participants’ hands. Under certain scheme structures, ESOP pay-outs are taxed as dividends. It is often important to manage the timing of receipts by the scheme itself, and on-distribution to employee beneficiaries to avoid any adverse tax implications.

Accounting for ESOPs

Similar to tax outcomes, the accounting outcomes are heavily dependent on the scheme structure. Generally though, ESOPs are either accounted for as a ‘share-based payment’ under IFRS2, or as an employee benefit under IAS19.

Under IFRS2, the ESOP investment is viewed as an option and depending on the scheme structure, the ESOP will be accounted for as an “equity-settled transaction” or a “cash-settled transaction”.

As equity-settled, an entity recognises a cost and corresponding entry in equity, based on the initial option valuation at the grant date, and there is no annual revaluation. As cash-settled, an entity recognises a cost and corresponding liability, based on the initial option valuation at the grant date. There is then annual revaluation to address changes in expected and actual outcomes.

Under IAS19, the cost of employee benefits is recognised in the same period employees earn them, resulting in relatively simpler accounting treatment.

Understanding the accounting implications of a proposed ESOP for the employing company and on consolidation is important.

ESOPs and Competition Commission: ESOPs in mergers and acquisitions

In reviewing a proposed merger transaction, the Competition Commission places a significant weighting on the “public interest” impact. In terms of “public interest”, among other things, the Competition Commission considers the promotion of a greater spread of ownership, in particular the levels of ownership by historically disadvantaged persons as well as workers.

Various deals have included an ESOP component, including Burger King; Coca-Cola Beverages; AB InBev; and PepsiCo. Based on engagement with the Competition Commission, ESOPs appear to be a favoured approach to achieving “public interest”, and are often included as a condition for approval.

Employee communication and trustee training

Critical to sustainable ESOP success is managing employee and, if relevant, union expectations. This can be best achieved through training and communication regarding scheme rules, business value drivers, and where necessary, basic financial literacy.

A well-designed communication programme supported by interactive participant sessions and easily understandable communication materials has a major positive impact on ESOP acceptance (reducing scepticism) as well as participants knowing what to expect, and when.

Of equal importance is ensuring that the trustees are empowered to confidently fulfil their fiduciary role. This requires that they have a good understanding of the ESOP workings, the business and drivers of success, as well as the role, duties and responsibilities of a trustee. This can be achieved through comprehensive trustee training.

Are you considering ESOP implementation?

ESOPs provide an attractive option to address B-BBEE ownership in a way that can achieve various other benefits at the same time.

If you are considering an ESOP for your business, it is imperative to critically investigate and analyse the structural options and related implications in order to identify what makes most sense for your business, while ensuring B-BBEE compliance.

To best managing employee expectations, simple and effective ESOP communications are important, together with trustee training.

With over 15 years of experience in ESOP design, execution, communication and trustee training, Transcend Capital can support you in identifying and implementing an optimal and sustainable ESOP solution.

About Shaun Smit CA(SA), MBA – Director at Transcend Capital

With over a decade of experience in providing Employee Share Ownership Plans (ESOP) and BEE transaction advisory to multinationals and South African corporates, Shaun Smit has a proven track record in crafting and executing ownership strategies aimed at fostering growth and sustained business success. Shaun believes that employee ownership can be a powerful tool for increasing engagement, improving business performance, and achieving meaningful broad-based empowerment. Outside of work, Shaun is a dad-taxi and enjoys running and playing tennis.

Shaun Smit

Director at Transcend Capital

Frequently Asked Questions

Can you improve B-BBEE scoring through an ESOP?

Yes, most companies in South Africa implement ESOPs to secure B-BBEE ownership credits and improve their B-BBEE status, while at the same time enabling benefit for their employees.

What are the B-BBEE requirements for an ESOP?

To recognise B-BBEE ownership via an ESOP, the main requirements include that employees must appoint at least 50% of the scheme fiduciaries (eg. trustees); employee beneficiaries must be clearly defined; there must be an annual general meeting of the ESOP; and on termination of the scheme any residual benefit must be distributed to the employee participants.

What percentage shareholding must an ESOP hold?

This depends on the company needs and objectives, but generally ESOPs hold between 5%–25% of equity.

Do employees need to pay for the shares in an ESOP?

In most ESOPs there is no requirement for employee to pay to participate in an ESOP. Funding is typically provided via vendor funding or external loans.

How long does an ESOP run for?

ESOPs can be structured to have a fixed life or to operate indefinitely, with the founding company having an ability to terminate the scheme.

What are the tax implications for an ESOP in South Africa?

For the implementing company, there are limited opportunities for tax deductibility, and the chosen ESOP funding structure may result in tax liabilities arising.

For employee participants, tax treatment is dependent on the scheme structure, and ESOP payments with either be taxed in the employees’ hands as dividends or income.

How is value distributed to employees in an ESOP?

Employees usually benefit through dividend distributions and/or capital appreciation after defined vesting periods. The founding company will determine the benefit structure and ESOP rules.

What are the accounting implications for an ESOP in South Africa?

The accounting outcomes depend on the scheme structure. ESOPs are typically either accounted for as a ‘share-based payment’ under IFRS2, or as an employee benefit under IAS19.

ESOPs and the Competition Commission’s Public Interest Considerations

Why are ESOPs in South Africa relatively uncommon?

Why Employee Ownership must be considered as part of your BEE strategy

Subscribe to The Transcend Capital Blog

Don’t miss out on the latest news and leading industry insights.